Riley: Progressive Magaziner and the Discount Rate

Michael G. Riley, GoLocalProv MINDSETTER™

Riley: Progressive Magaziner and the Discount Rate

The discount rate is, in theory, determined in large part by the yield curve and the prevailing risk free rates. In 1997 rates were significantly higher and so it was a fairly easy to promise to achieve 8% returns without much risk. As can be seen in the chart below the 10 year risk free rate was 6.5% and the 30 year risk free rate was close to 7%. Had the retirement board simply invested in zero coupon bonds at 6.8% in the 1990’s, going forward they would almost fully guarantee normal cost funding.

But the rate scenario can change and, generally speaking, the lower the risk free discount rates the lower expected returns are on all risky assets. Stocks are the riskiest of the asset classes and, as such, most fiduciaries, like the State of Rhode Island, have roughly 55 to 65% invested stocks and the remainder in fixed income and alternatives.

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLASTInterest Rates in 2015

Last year was the fifth year of extraordinary federal monetary intervention and we are still operating under ZIRP (zero interest rate policy). Given those facts, a super majority of U.S. economists and money managers are predicting much lower returns on their portfolios. Now rates look like this:

Last year’s 2014 RI Treasurer Debates with Ernie Almonte, Seth Magaziner, and Frank Caprio featured Seth Magaziner declaring he that was a superior money manager and also stated he would “raise” the discount rate. In my opinion “RAISING” the discount rate from 7.5% would be truly insane and serve no public purpose but is completely in line with his senior policy advisor Tom Sgouros who believes that Gina Raimondo created a “false crisis” by lowering the rate to 7.5% during the 2011 Pension reform.

If Treasurer Magaziner were to make that move to raise the discount rate, it would lower the budgeted amount necessary for funding the pension plan in 2016, 2017 etc. and make it easier to spend on other things or fill budget holes like lost casino revenue. Once in effect, both Magaziner and Raimondo would be happy and could better balance the near term State budget by kicking the can and placing an even larger burden on the next generation.

This would be completely irresponsible, yet not unheard of in Progressive thought, which increasingly seems to be Governor Raimondo’s path. If she does in fact believe that a lower discount rate was necessary in 2011 then there is even more evidence today that it remains too high and should be moved toward Warren Buffett's 6%. Regardless, both GASB 68 and Moody’s will ignore Magaziner‘s rookie guess and use rates approaching 5.4% in calculating unfunded liabilities.

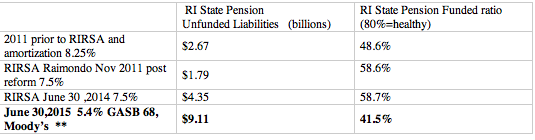

New Liability figure explodes

Here‘s what the new funded ratio in Rhode Island will look like in just 3 months when fiscal year 2015 comes to an end.

**Assumes 2.5% fy 2015 return on assets

Even under reform and after a massive bull market the funded ratio has not improved. That means costs have been calculated incorrectly and discounted incorrectly. Using GASB 68, the State and Magaziner will be forced to report a collapse in the funded ratio and a huge increase in liability. Under current law, the state does not have to fund reality but they do need to show a 5 year plan and clearly spell out the current financial condition of the state. That should be interesting.