EXCLUSIVE: Providence Pensions—Costs to Triple in 20 Years

Stephen Beale, GoLocalProv News Editor

EXCLUSIVE: Providence Pensions—Costs to Triple in 20 Years

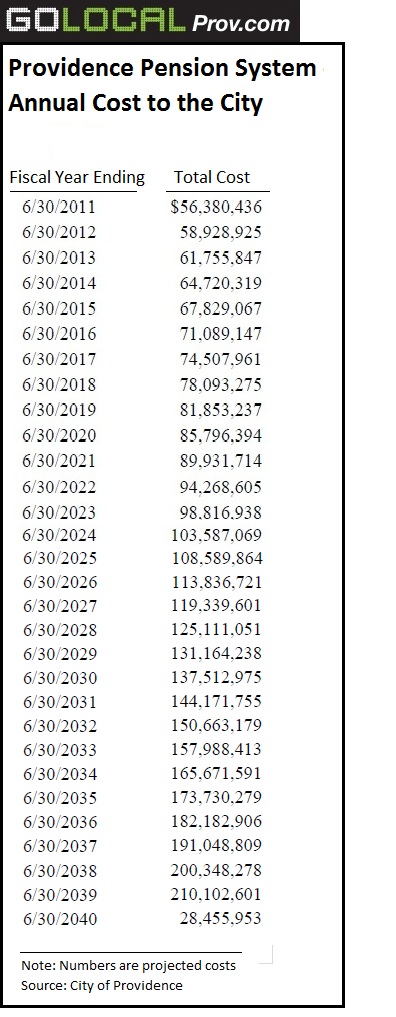

Providence can catch up to that unfunded liability, but at a big cost. The study shows that the annual cost—known as the Annual Required Contribution, or ARC—will soar from $56.3 million in the current year to $144.1 million in 2031. Just five years after that, it will be $182.1 million.

“It is sustainable? No, in my opinion it is not sustainable,” said City Councilman David Salvatore. “We can stop the bleeding now by bringing some amendments to the charter and the retirement code.”

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLASTCicilline ‘left a big mess for Angel Taveras’

Councilman Miguel Luna blamed former Providence Mayor David Cicilline for not fixing the system when he had the chance. “When there were times he could have done something to get us out of the hole, he took no action,” Luna said. “He left a big mess for Angel Taveras.”

The new study, which was prepared by Buck Consultants, shows that the pension fund had a total liability of $1.25 billion, with assets estimated at $427.8 million, as of June 30, 2010. That left the system 65.94 percent unfunded. The year before, the system had an unfunded liability of $804.7 million but was 66.5 percent unfunded, since its assets were also lower then.

The 45-page report also documents in detail the extent to which many longtime retirees are collecting compounded cost of living adjustments, or COLAs—which have been cited as a major reason for the rising costs of the retirement system. For example, 278 police officers who retired before 1990 are receiving a 5 percent COLA and 265 firefighters who retired during the same period also are benefiting from the same rate. Those COLAs were later reduced to 3 percent for newer retirees, but those are still compounded.

Solutions range from bonding liability to 401(k)s

Both Luna and fellow Councilman Luis Aponte suggested that the city made a mistake when the Cicilline administration decided against bonding all of the unfunded liability. Luna said the annual cost of paying back the bond would have been closer to $45 million, rather than the $56.3 million in pension contributions the city owes this year. Plus, he said the amount would have remained stable over the long term.

“We tend to look at this in snapshots and I think that tends to limit your options,” Aponte added. “You need to look at this as it is—it is a long-term investment strategy.”

Over the next 10 to 20 years, as the older compounded COLAs of 5 percent are phased out, Aponte said the costs will become more predictable, making it easier to plan for the long term.

He said the city should consider raising the amount that employees contribute and decreasing how much it pays into the system. In 2010, employees contributed $10.8 million into the system while the city poured in $50.2 million, according to data in the report.

Aponte is less optimistic that a 401(k) approach would work, since the system needs current employees to continue to pay into the fund to support the benefits of retirees. But Salvatore said it would be practical to put new hires into a hybrid system that combines elements of a 401(k) with a traditional public employee pension. “With the fluctuations in the stock market, you wouldn’t want all the employees to put their eggs in one basket,” Salvatore said.

Salvatore said the city should also consider raising the retirement age, saying that the pension system was never meant to allow someone to retire in their 40s and collect pensions for the next 30 years.

Union Leader: Don’t kick the can down the road

For Paul Doughty, President of the International Association of Fire Fighters, Local 799, said the key number to keep an eye on is not the rising unfunded liability—but the city’s annual required contribution. That liability will decrease if the city makes its annual contributions to the fund.

“We either need to stick to it, or change the plan,” Doughty said. “If we keep turning a blind eye and saying we only need to put in $40 million when you need $50 million—that only compounds the problem.”

“We need to pass a law or ordinance that you have to put the money in,” he added. “Otherwise, you’re kicking the can down the road.”

Providence is currently in the second year of a 30-year amortization schedule. Doughty acknowledges that sticking to the plan will be costly. He says it may be worthwhile to consider extending that period to 40 or even 50 years. But that time to do that is now, not in the future, he says.

Taveras, for one, intends on paying 100 percent of what the city owes to the pension fund in his first budget, according to his spokesman.