Michael Riley: Providence Vying for Worst Funded City in America

Michael G. Riley, GoLocalProv MINDSETTER™

Michael Riley: Providence Vying for Worst Funded City in America

Last week, Moody’s Credit Rating Agency, using new metrics that should surprise no one, unceremoniously dropped Chicago three notches to BAA1. This is three levels above junk and affects $8 billion in GO (General Obligation Bond) debt. Similarly, Providence is also rated BAA1 but that was done in September 2013 prior to Moody’s change in methodology and after Providence’s mild reform effort. The difference between Mayor Taveras of Providence and Rahm Emanuel as individuals is obvious. One mayor is aggressively seeks a solution to an impending calamity and the other Mayor tinkered, caved to union demands and is done, thereby dooming Providence to receivership. Mayor Emanuel thinks the city of Chicago is in dire straits, is pushing the unions, and is looking for solutions. Mayor Taveras has fooled around with the accounting; made the laughably courageous call to end 6% COLAs (Cost of Living Adjustments) and now now everything is fine.

From Moody’s perspective, they both have ratings that fairly “reflect the city’s massive and growing unfunded pension liabilities, which threaten the city’s fiscal solvency absent major revenue and other budgetary adjustments adopted in the near term and sustained for years to come.”

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLASTMayor Emanuel has resorted to taxable bonds for funding the city and Providence’s next Mayor may adopt this tactic. But unless both cities can significantly renegotiate the contracts with their respective unions soon and raise taxes, they both have very few options other than Bankruptcy or receivership.

Did Providence mislead bondholders and citizens?

In Providence there is an additional issue of answering charges that Providence has mislead bondholders and citizens by false and inflated reporting of assets in the pension plan. We were the first in the country to expose this and we are awaiting an answer. Calls to Segal, who recommended Providence discontinue their practice in the audit produced a few weeks ago, have not been returned. We have studied hundreds of cities nationwide, especially poorly funded pension plans and have been unable to find similar asset treatment that used by Providence officials and their accountants.

In July 2013, Miami and its former budget director were charged with securities fraud related to several municipal bond offerings. The SEC alleged that misleading financial information was given to investors. My readings of the last few reports from Providence to its citizens and to the RI Municipal Pension Study Commission show that their numbers will require significant changes to comply with regulators and ratings agencies. Pensions and accounting can no longer be swept under the rug. Providence will have to explain its accounting treatment for assets in the plan and why the auditor told them just a few weeks ago, to end those accounting practices.

An interesting battle in Coventry

Rhode Island has already begun implementing an interesting municipal incentive program known as RIGL 45-13.2-5 and 2-6. This program seeks to reward good behavior in pension management by localities. Coventry believes it deserves its share of “incentive”, approximately $166,000 out of a $5 million program. The idea of the program is to encourage local pension plans to reform and/or join the state pension system. Coventry’s Town Council and town manager argue that the dispute over the $20 million of liability in non-certified school employees should not affect this aid. The town believes the liability and the lack of solution are the schools problem and not the town’s problem. The town has been contributing their required amount for decades. The interesting juxtaposition of funding responsibilities and obligations has created quite a stir and the town of Coventry believes that the state and revenue director may be acting “unlawfully” by withholding aid from Coventry. Coventry claims it is the only town that has had aid withheld. This is especially surprising considering the wide range of compliance and talks associated with Funding Improvement Plans.

From Coventry Town manager Thomas Hoover:

Mr. Hoover said it is very curious to the town that the Town of Coventry is the “only one” in the State of Rhode Island that this has been withheld from. He said the town is working on this issue; however he cannot say that the town is at a conclusion on their discussions, but they are continuing to talk. Mr. Hoover said as you can see from his letter, he is hopeful that the Department of Revenue and the Governor changes their position on the municipal aid since the town is adamantly against the action that was taken, and he said “it not only is it unfair, but the town believes it is unlawful.

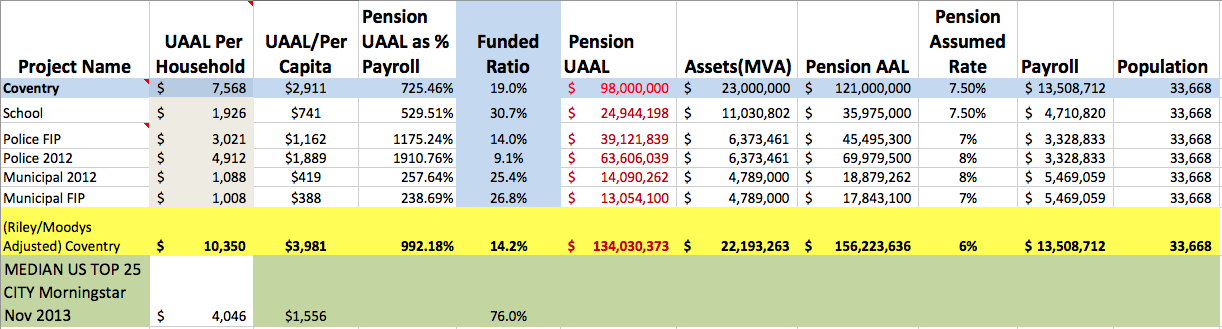

While this is all very interesting, it doesn’t change the math and Coventry will be unlikely to make it to year-end 2014 without a receiver. The town awaits a huge arbitration ruling on a police contract that may render this whole discussion mute and trigger bankruptcy. We should know by the end of this month. In addition, the town understates its liabilities by about $64 million. We show Coventry’s Unfunded Pension Liability as $134,000,000 using Moody’s and GASB 2014 metrics. We also have not included the effects of the liability of CCFD liquidation, which is in the tens of millions.

Coventry's Unfunded Pension Liability

Source: Pension and OPEB Study Commission

In addition, Mr. Hoover said it is very curious that the Town of Coventry is the “only one” in Rhode Island that this has been withheld from. He said the town is working on this issue; however he cannot say that the town is at a conclusion on their discussions, but they are continuing to talk. Mr. Hoover said, as you can see from his letter, he is hopeful that the Department of Revenue and the Governor changes their position on the municipal aid since the town is adamantly against the action that was taken. He also said, “it not only is it unfair, but the town believes it is unlawful.”

Providence Pension Liability

Unfunded Liability in 2013

Total Liability: $1.2 billion

Actuarial Assets: $380.4 million

Unfunded Liability: $831.5 million

Unfunded Liability in 2011

Total Liability: $1.2 billion

Actuarial Assets: $380.4 million

Unfunded Liability: $831.5 million

Percent Funded in 2013

Funding Ratio: The ratio of the amount of actuarial assets to the amount owed.

Funding ratio in 2013: 31.39%

Percent unfunded in 2013: 68.61%

Percent Funded in 2011

Funding Ratio: The ratio of the amount of actuarial assets to the amount owed.

Funding ratio in 2011: 31.94%

Percent unfunded in 2011: 68.06%

Rate of Return

Former Assumed Rate of Return: 8.5%

New Assumed Rate of Return: 8.25%

What the state’s assumed rate of return is: 7.5%

What Moody’s Investors Service says the assumed rate of return should be: 5.5%

What investor Warren Buffet says the assumed rate of return should be: 6%

Actual Return on Investment

Actual Market Return in FY 2012: 1.49%

Actual Market Return in FY 2013: 11.35%

Current Assumed Rate of Return: 6.42%

Average Market Rate of Return for FY 12 and FY 13: 8.25%

Impact of Lower Rates of Return

$72 million:The city unfunded liability increased by this amount when the city lowered its assumed rate of return by a quarter of a percentage point, from 8.5% to 8.25%

$506.2 million: The estimated increase in the unfunded liability were the city to use the 6% assumed rate of return recommended by Moody’s Investors Service.

Retiree Pay – Fire and Police

Number on Active Duty: 834

Average Annual Pay: $61,325

Number of Retirees: 587

Average Retiree Age: 65.3

Average Retiree Annual Pay: $40,512

Disability Pensions – Fire and Police

Number on Disability: 418

Average Age: 64.8

Average Annual Pay: $59,028

Retiree Pay – Other City Workers

Number of City Workers: 2,164

Average Annual Pay: $38,687

Number of Retirees: 1,453

Average Retiree Age: 72

Average Retiree Annual Pay: $18,252

Disability Pensions – Other City Workers

Number on Disability: 88

Average Age: 66.8

Average Annual Pay: $18,684

Current Cost of Pension Fund

For 2013

City Contribution: $58.1 million

Employees Contribution: $10.9 million

Net Investment Return: $18.1 million

Cost of Retiree Benefits: $95.4 million

Note: Net investment return is the return on investments after investment and administrative fees have been paid.

Cost of Pension Fund in 10 Years

Normal Cost: $9.8 million

Additional Cost Because

of Unfunded Liability: $84 million

Total Annual Cost: $94.3 million

Note: Total figure for the year includes a small second payment for the deferred liability.

Cost of Pension Fund in 20 Years

Normal Cost: $13.9 million

Additional Cost Because

of Unfunded Liability: $118.5 million

Total Cost: $132.4 million

Paying Off Unfunded Liability

Average annual increase: 3.5%

Number of additional years to pay off: 27

Fiscal year unfunded liability to be paid off by: 2040