EXCLUSIVE: Diocese of Providence's Teachers & Staff Pension Fund Faces Failure, May Impact Thousands

GoLocalProv News Team

EXCLUSIVE: Diocese of Providence's Teachers & Staff Pension Fund Faces Failure, May Impact Thousands

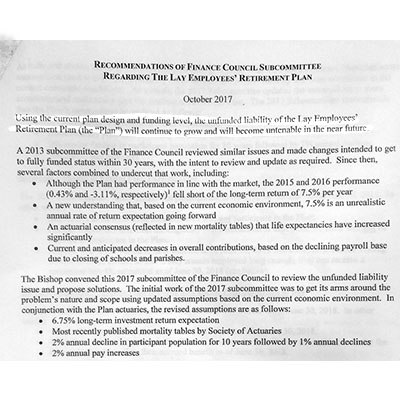

“The unfunded liability of the Lay Employees’ Retirement Plan will continue to grow and will become untenable in the near future,” states a recent Diocesan document.

The document, entitled, “Recommendation of Finance Council Subcommittee Regarding the Law Employees’ Retirement Plan," dated October 2017, paints a bleak future for the fund, outlines the causes of the fund’s tenuous structure, and calls for immediate action to stabilize the fund.

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLASTThe Diocese refused to respond to questions.

Latest Revelation of Diocesan Pension Problems

A second document also secured by GoLocal, which was prepared by the Diocese top financial officers -- Monsignor Raymond Bastia and Chief Financial Officer Michael Sabatino -- is to be considered by top Diocesan officials at a meeting scheduled for this week with Bishop Thomas Tobin.

The document is dated June 19, 2018, and marked “immediate action” and it calls for drastic cuts to beneficiaries of the fund. Also, to be considered at the meeting is the October 2017 recommendation document and the plan outlined is to be considered for action this week.

Another dire statement in the report says, "Even with the revised more realistic assumptions, if we make these changes, it will still take 30-35 years to fully fund the Plan."

The impact for those presently in the plan is sweeping. One of the hardest hit are those now working but who have not vested in the fund. To be eligible, an employee must have worked for ten years.

The impact on those non-vested staffers is that they will lose all of the pension contributions made into their accounts if the plan is approved. Other big impacts are the fund will be frozen and fund members wanting to exit the fund, who may be concerned that the fund will collapse, could be allowed to exit -- but will take a 40 percent cut to their lump sum payment.

For a nine-year teacher who has taught for nine years and had an annual average salary of $50,000 over those years, they would have accrued an estimated $54,000, but under the plan to be adopted by the Diocese -- that teacher will receive zero.

The October recommendation document which is up for consideration this week cites four primary reasons why the plan is unstable:

Although the Plan has had performance in line with the market, the 2015 and 2016 performance (0.43% and -3.11%, respectively) fell short of the long-term return of 7.5% per year.

A new understanding that, based on current economic environment, 7.5% is an unrealistic annual rate of return expectation going forward

An actuarial consensus (reflected in mortality tables) that life expectancies have increased significantly

Currently and anticipated decreases in overall contribution, based on the declining payroll base due to closing of schools and parishes.

The four primary reasons for the plan's lack of stability have been conditions for years. Catholic schools in Rhode Island have been closing for the last three decades, the 7.5 percent annual rate of return has not been considered achievable for the better part of a decade, and the major changes in mortality rates was achieved decades ago.

The critical need to immediately act on to change the fund raises questions about the “Church Plan’s” actual viability.

The August 2017, the St. Joseph Pension Fund collapsed leaving more than 2,700 plan members of the fund facing a shortfall of $118 million to fully pay their benefits. That pension fund failure is now being litigated in both federal and state courts. The receiver for the pension fund is alleging in the suit that the Diocese and fifteen other defendants are guilty of financial fraud.

So-called “Church Plans” are unregulated by the state and federal agencies and do not require the managing religious organizations to provide reporting of the fund’s performance to the members.

The June 19 document outlines a plan that has significant impact on hundreds of teachers and staff now working for the Diocese and the related schools who participate in the fund, as well as, as many as thousands of plan retirees.

According to the documents, “It is strongly recommended for the reasons outlined in the Subcommittee document of October 2017 that the present Lay Employee Defined Benefit Plan be frozen on or before 12/31/18.”

“Simultaneous to the freeze of the DB [Defined Benefit] Plan a new Defined Contribution Plan should be created by using the existing 403(b) plan as the platform, with modifications. New DC Plan to use 2% of the payroll contributions towards an employer contribution to the DC plan.”

Presently, each of the member schools makes a 12 percent contribution to the fund on behalf of their respective employees, but under the new plan, which is expected to be implemented, the schools (which include Bishop Hendricken, St. Raphael, and Prout School, as well as many of the Catholic middle and elementary schools) will continue to be required to make the contribution of 12 percent, but 10 percent will go to stabilizing the fledgling fund and 2 percent will go into a, de facto, new fund.

Has the Church Been Misleading Employees and Member Schools?

Behind the scenes, the Diocese’s financial staff has been scrambling for the past year to stave off a near-term collapse of the fund, and the public relations of the church has been communicating stable performance of the Diocese’s finances.

“The annual audit of its finances shows the Diocese of Providence closed out fiscal year 2016/2017 in a stable position thanks to a growing economy that has produced strong returns on its investments coupled with a successful Catholic Charity Appeal last spring," wrote Rick Snizek, Executive Editor of the Rhode Island Catholic.

“All of these factors were helpful to our diocese as we remain faithful to the mission of evangelization and to our joy-filled commitment to the many corporal and spiritual works of mercy that we provide to the people of our state and beyond,” said Bishop Thomas J. Tobin in a statement announcing the report, which was examined by the independent auditing firm Mayer, Hoffman and McCann, P.C., and reviewed and accepted by the Diocesan Finance Council.

Trouble for Diocesan Lay Employees’ Retirement Plan Cropped Up in 2009

There have been early signs of trouble dating back to 2010. GoLocal reported in September of 2017:

According to a 2009 article in the Diocese of Providence’s newspaper, Rhode Island Catholic, the Lay Employees’ Retirement Plan was in distress and the benefits payouts were being cut back.

The then-administrative secretary to the Lay Employees’ fund, J. Timothy Kocab, administrative secretary of the Lay Employees’ Retirement Board said, “The plan’s assets…have declined significantly in value during the past several months.”

In addition, Kocab is quoted as saying, "These are necessary steps in order for us to refocus our resources on strengthening the funding position of the Lay Employees’ Retirement Plan.”

Kocab told Diocesan employees in a letter, "Your employer remains committed to helping you build financial security for your retirement years.”

In September, the Diocese fiscal office refused to answer questions about the St. Joseph pension fund bankruptcy, the Lay Employees’ Retirement Fund, or any other church funds associated with the Diocese of Providence.

According to the Diocese’s website, the fiscal office was “established in 1973 to assist the Roman Catholic Bishop of Providence and related Diocesan Corporations in their administration of the temporal resources of the Church, the Fiscal Office operates in a multi-corporate environment and is responsible for the day to day activity of some 30 separate internal corporations.”

The details of the 2017 draft plan, which was the result of the Bishop convening the 2017 subcommittee of the Finance Council to review the unfunded liability issue and propose solutions, contain the initial work of the 2017 subcommittee whose task was to get its arms around the problem's nature and scope using updated assumptions based on the current economic environment.

As stated in the documents:

In conjunction with the Plan actuaries, the revised assumptions are as follows:

* 6.75% long-term investment return expectations

* Most recently published mortality tables by Society of Actuaries

* 2% annual decline in participant population for 10 years followed by 1% declines

* 2% annual pay increases

Under these revised assumptions, it is understood, that unless we increase contributions by nearly 15% - and there is no appetite for that - the Plan is likely to become insolvent before 2047. Therefore, the 2017 Subcommittee also is recommending:

* A full freeze of the Plan (no new participants are accruals)

* No change to benefits of folks that have retired

* No change to accrued benefits through the date of the freeze

* No change to payroll contributions (remains at 12% of the full-time payroll)

* Amed the withdrawal liability provisions of the Plan to require approval for any employer to withdraw after the freeze

* Offer a voluntary discounted lump-sum buyout to certain participants

* Fund a partial replacement defined contribution benefit

Even with the revised more realistic assumptions, if we make these changes, it will still take 30-35 years to fully fund the Plan.