Transparency Denied: New Treasurer Censors Hedge Fund Reports

Stephen Beale, GoLocalProv News Contributor

Transparency Denied: New Treasurer Censors Hedge Fund Reports

In a letter to GoLocalProv, Magaziner’s office said that information considered confidential or trade secrets had been redacted. In a statement, spokeswoman Shana Autiello said that the office was relying on the Attorney General Peter Kilmartin’s decision in 2013 that the state public records law did not require then-Treasurer Raimondo to release uncensored copies of the reports to the Providence Journal.

When he was running for office, Magaziner promised greater transparency. He made a point of mentioning it on the Issues section on his Web site and, elaborated on it in one media interview, saying he would see what he could do to release more information about the hedge funds and explore the possibility of re-negotiating the agreements that limited what state officials could make public.

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLAST“It’s very disappointing that he hasn’t reversed the old treasurer’s decision, consistent with his campaign promise,” said Edward Siedle, a Forbes.com contributor who conducted his own investigation into the state pension fund’s lack of transparency and investment decisions under Raimondo. Siedle said that Magaziner had opted to continue Raimondo’s “flawed secrecy policy.”

“It appears the new treasurer is not going to be more transparent than the last treasurer,” Siedle said. All of which, he added, begs the question as to who is benefiting, Wall Street or the public employees whose retirement savings are being invested.

“Whose interests [is] he seeking to protect?” Siedle concluded.

Soon after taking office, Raimondo implemented a deliberate strategy of moving what ended up being $1 billion in pension money into hedge funds. The move was controversial—not only because of the high fees charged by hedge fund managers, but also because the returns ended up underperforming the market. In fiscal year 2012, the pension fund lost $200 million under the new investment strategy.

The Due Diligence reports are important because they are the documents that the State Investment Commission, under Raimondo’s leadership, used to evaluate the hedge funds before making investment decisions.

The reports contain reams of vital information including: the structure and leadership of the funds, staff compensation, the extent to which they are deemed in compliance with federal regulations, how they make investment decisions and protect their investors, and how the fund is valued. The reports were prepared by Cliffwater, a third-party investment adviser that is under contract with the state. (Cliffwater CEO Stephen Nesbitt did not respond to a request for comment.)

In 2013, the Providence Journal requested copies of the Due Diligence reports for 19 hedge funds. (In all, there were 38 reports—two for each fund. One covers investments; the other fund operations.) When her office refused to release the complete reports, a coalition of open groups sent a protest letter, saying the state public records law (known by the acronym APRA) had not been properly applied.

Leaders of two of those groups this week told GoLocalProv they were disappointed the lack of transparency is continuing.

“The ACLU continues to have many of the same transparency concerns that we, along with others, raised with then-General Treasurer Raimondo about this issue two years ago,” said Steve Brown, executive director of the ACLU of Rhode Island. “Some of the redactions may very well include information properly deemed confidential under APRA. However, when dealing with the investment of taxpayer money, public agencies should always err on the side of disclosure, not secrecy, if there is any doubt.”

Secret meetings and hidden staff

Magaziner’s spokeswoman said that his office was contractually bound to not release the information. “It is the position of this office that previous contracts must be honored. Treasurer Magaziner will continue to be as transparent as possible without undercutting the ability of funds to deliver the best possible returns for our state,” Autiello said.

She did not say whether Magazine had attempted to re-negotiate the agreements or explored the legal and financial ramifications of breaking them—possibilities he had aired while on the campaign trail.

Invoking the contracts, however, is likely not to satisfy open government advocates. In their August 7, 2013 letter to Raimondo they declared that, “we firmly reject the view that a public body has the authority to contractually waive the statutory rights that the General Assembly has provided the public under APRA. Allowing agencies to do so would open a gaping hole in the Act and frustrate its core purpose. If certain records are exempt from disclosure, it is because APRA, not a contract, makes them so.” (Besides the ACLU and Common Cause, two other signatory groups were the Rhode Island Press Association and the League of Women Voters.)

A GoLocalProv review of the reports shows every single one has numerous redactions. In some cases nearly whole pages are blacked out. And, it is often difficult to tell why the information would be considered confidential or fall under the category of trade secrets. In every report the scores that Cliffwater gave the hedge funds—on everything from their compliance with federal regulations to their business management—are redacted.

On a number of the reports some employee names, positions, and backgrounds are provided while some of the same information for their coworkers is blacked out. One report redacted the dates and locations of meetings between Cliffwater representatives and officials at the hedge fund they were evaluating. Another report even redacted some of the information in a glossary of terms.

“[A] few of the particular redactions that have been made—such as the apparent random deletion of the names of a handful of key fund employees—are highly suspect, and can serve only to raise questions about the validity of the redaction process as a whole,” said Brown.

As surprising as some of the redactions are, so is their inconsistency. While one report contains no unredacted information on meetings others at least disclose the date and locations if not the names of the participants. Employee names are withheld, but not in any consistent pattern.

When asked whether hedge funds had made the redactions themselves, Autiello would only say that the Treasurer’s office had stuck to its practice of making “final redactions.” In one report it was apparent that there had been two rounds of redactions—one with made on the original document with a marker, the other electronically.

The possibility that hedge fund managers made decisions on what information would be made public has alarmed open government advocates.

“We are aware of nothing in the Access to Public Records Act that authorizes an agency to delegate to private entities the decision as to what records are available to the public under the Act,” their 2013 letter states. “APRA would be seriously undermined if any record submitted by a private party to a government agency [was] subject to withholding based on the third party’s interpretation of the open records law and its view of what should be disclosed to the public.”

Magaziner’s office did not provide any explanations for why some seemingly non-confidential information, such as employee names, was withheld, but one local investment professional said there could be a legitimate reason. “Certain employees and their compensation should not be revealed due to poaching,” said Mike Riley, the managing member of Coastal Management Group, LLC and also the manager of a small hedge fund, Narragansett Multi-Strategy Fund. (No state pension money is in the fund, according to Riley.)

Riley, who is also a GoLocalProv MINDSETTER, was asked if, in his opinion, the information redacted in the reports was indeed confidential or pertained to trade secrets. He said it was. In particular, after reviewing one set of reports, for Ascend Capital, he said the redacted sections contained information about how the firm makes its money.

Nonetheless, he said the reports for Ascend Capital still allowed someone to determine their fee structure—information which should be public, according to Riley. “I’m absolutely in favor of as much transparency as possible. Fees are absolutely a necessary disclosure,” Riley said. “But I do side with the hedge funds on some of the proprietary information.”

“In summary, the reports—even in redacted form—are thorough and tell me enough to make an investment decision and-or opine about the appropriateness of the investment and the level of fees,” Riley said.

Video Wall courtesy of Harmonica Pete/ flickr

Hedge Fund Reports Censored

Hedge Fund Performance

Investment Due Diligence Report

August 2011

Hedge Fund: Ascend Partners Fund I and II

Description: The image on the left is from Page 10 of the 17-page due diligence report on Ascend Partners prepared by Cliffwater Associates for the State Investment Commission. In the selected excerpt, just about all the information pertaining to the performance of the hedge fund has been redacted. The section preceding the table states that the second fund launched by the firm had an annualized return of 8.12 percent. The redacted exhibit is said to contain “more detailed performance data” including “statistics pertaining to more recent returns.”

Secret Scores

Operations Due Diligence Report

September 2010

Hedge Fund: Ascend Partners Fund I and II

Description: To the left, is the top of the second page in the due diligence report Cliffwater prepared on Ascend Partners. As the context makes clear, no actual proprietary information about the fund itself is discussed in the page. Instead, the “scores” that a reviewer at Cliffwater gave to the hedge fund—on everything from business to risk management are redacted. Even the name of the fund’s external administrator is withheld.

No Simple Yes or No

September 2010

Hedge Fund: Ascend Partners Fund I and II

Description: To the left, is the third page of the same document from the preceding slide. The table appears to be a standard form that Cliffwater uses in its evaluation of all hedge funds. Note that the redactions encompass critical information about the fund’s compliance with SEC regulations and the protections it has for investors—in this case, state retirees. Not only are the standard measures it employs blacked out, but whether the hedge fund meets those measures—a simple “yes” or “no” is blocked too.

Veiled Valuation

Operations Due Diligence Report

September 2010

Hedge Fund: Ascend Partners Fund I and II

Description: The valuation process is critical to determining the value of one’s investments. The redacted excerpt shown to the left briefly explains that the hedge fund does not determine the own valuations. Instead, those are determined by third-party services. The report purports to give an example of one of those services. But apparently that too is considered confidential information by state authorities. Notably, even though the hedge fund does not have a valuation committee, the section on the next page about the valuation committee members is still redacted.

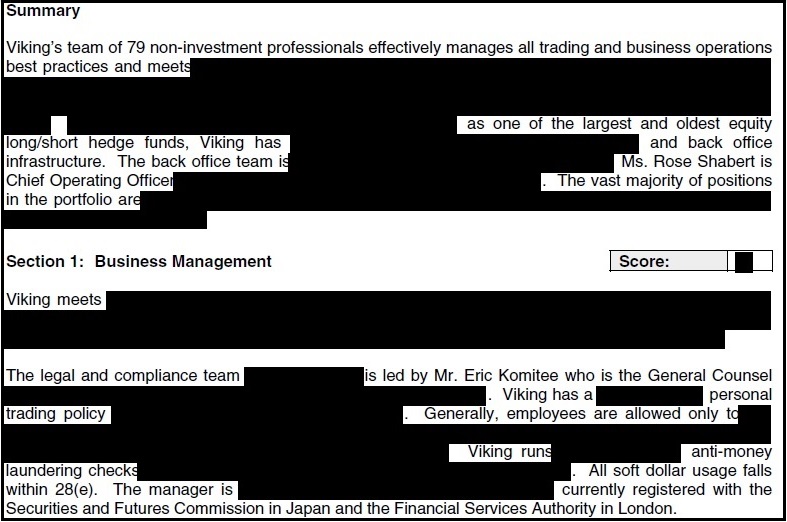

Short Summary

Operations Due Diligence Report

November 2010

Hedge Fund: Viking Global Equities

Description: The summary section for most due diligence reports on hedge fund operations are usually the least redacted portions of the reports, but not here, where so much has been redacted it’s nearly impossible to infer anything about the information that has been withheld.

Behind Closed Doors

Operations Due Diligence Report

November 2010

Hedge Fund: Viking Global Equities

Description: The redactions to the left again raise the question as to how trade secrets and proprietary information are defined by the state Treasurer’s office. Here even attendees at meetings between Cliffwater, the state’s investment adviser, and the managers of the hedge fund under review are blacked out.

No Name Partners

Investment Due Diligence Report

January 2011

Hedge Fund: Third Point Partners

Description: Under the state’s interpretation of confidentiality rules it is apparently permissible to name the CEO but not his partners. GoLocalProv checked the firm’s Web site and its current partners who compromise the executive team—including their education and prior experience—are listed. But none of their backgrounds matched those of the partners mentioned here. None of which explains why the names are redacted.

What Risk?

Investment Due Diligence Report

January 2011

Hedge Fund: Third Point Partners

Description: To the left is what appears at the top of Page 11 in a 23-page report on investment performance and management by Third Point Partners. The two blocks shown here are in a series of black boxes which supposedly contains examples of the firm’s investment strategy. Here even the subhead describing the investment is partially redacted.

Three Strikes

Investment Due Diligence Report

July 2011

Hedge Fund: Winton Capital Management

Description: Many of the redactions are as surprising for what is redacted as for what is revealed. In this table of key staff at Winton Capital Management, most are listed, along with their years of experience and their educational background. The table even notes that the second-in-command position at the firm is occupied by the nephew of its chairman and founder. But three names are deleted for no apparent reason. Were these employees fired? Or did they leave for other work? Either way does such information fall under the category of trade secrets or proprietary information?

Dark Money

Investment Due Diligence Report

July 2011

Hedge Fund: Winton Capital Management

Description: One can understand why a hedge fund might not want to disclose details of how it compensates its staff—as that is the primary means of incentivizing high performance among employees. But what about the public’s right to know? Or the right of state employees to know whether their pension savings are supporting outrageously high bonuses for hedge fund executives?