Rhode Island's Foreclosure Crisis Far From Over

Dean Starkman, GoLocalProv News Editor

Rhode Island's Foreclosure Crisis Far From Over

The latest numbers, obtained by GoLocalProv from Rhode Island Housing, the state housing agency, show new foreclosures actually ticking up slightly in the first three months of 2013, the latest data available, adding to the pipeline of foreclosure to come.

Meanwhile, the number of mortgage delinquencies—the prelude to foreclosure—is projected to rise for the rest of the year before finally dropping off. A real recovery? That’s two years away. Normalcy in the housing sector? Come back in 2018.

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLAST“The battle has just begun,” says George Babcock, a leading foreclosure attorney based in Pawtucket. “What happens here only a daily basis...the mortgage nightmare is incomprehensible to me.”

Uptick in latest foreclosure figures

While overall mortgage delinquencies and foreclosures in the state are off their disastrous peaks from a couple of years again and slowly heading down, measures of housing misery remain at stunningly high levels historically and continue to outpace both the New England and national averages. According to the latest Rhode Island Housing data, total loans in foreclosure hit 3.89 percent of all mortgages in the state, up slightly from the previous quarter and down slightly from the same quarter a year ago. At 7.71 percent, the state’s total delinquencies were down slightly from the previous quarter and up slightly for the year. Rhode Island continued to lead New England with the worst delinquency rate and is the 12th worst in the nation. A staff-generated projection of state delinquencies rates shows them rising to over 8.5 percent by the end of the year before dropping below current levels in the first quarter of 2014.

“God has put me through a lot with this house,” she says.

Duped into a disastrous loan

She never wanted the massive (to her) $244,000 mortgage in the first place—not after she saw around the time of the closing that the monthly payments would come to more than $1,800 a month, a huge portion of the salary she draws working in the state Department of Motor Vehicles. But, she says, a loan officer warned her that the sellers would “‘sue you if you back out of this.’” Briggs learned only later that there was no legal basis for such a threat.

The payments stretched her income to the point that she had wait to pay until after the second of her semi-monthly checks arrived, forcing her to factor in a $76 late fee every month. When the water tank broke and the sewer backed up, there was no margin for error. Within a few months of buying the home in 2006 she fell behind.

Rhode Island, national delinquencies remain high

To be sure, the trends overall in foreclosures all point down from the historic levels reached after the financial crisis that followed the fall of Wall Street giant Lehman Brothers in September 2008. For decades, loans in foreclosure in Rhode Island (and elsewhere) typically ran to a fraction of a single percentage point, with changes measured in a few hundredths of a percentage point, known as “basis points.” At the peak of post-crisis fallout, early 2011, loans in foreclosure amounted to fully 4.5 percent of all loans in the state, while delinquencies—loans with payments 60 days past due, peaked at nearly 9.5 percent, according to Rhode Island Housing figures.

To see RI Housing graphs describing Rhode Island's foreclosures, go here.

Big human toll

But, the reality is that fluctuations of delinquencies and foreclosure data from month-to-month or even year-to-year mask a larger picture of a single, slow-motion train wreck in the housing sector that has already upended thousands of lives, set back low-income communities, hollowed out whole neighborhoods, and, worst of all, still has years to play out. The impact just on the state and its economic prospects, for instance, are profound and still not yet fully understood. A survey a couple of years ago showed that Rhode Island families had already suffered $5.6 billion in lost wealth in just the first two years of the crisis.

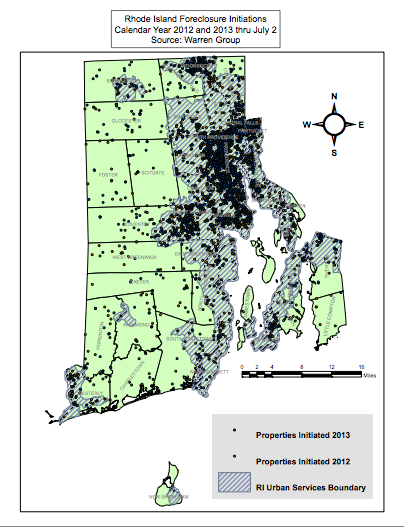

And while most of the new foreclosures were started, as would be expected, in Providence and the rest of the state’s urban core, even the more affluent suburbs have not been immune. Cranston and Warwick, for instance, contribute more than 21 percent of the 967 newest foreclosures among what the state calls its 12 Hardest High Fund communities, those eligible for state and federal housing assistance, according to Rhode Island Housing figures.

In an interview, Richard Godfrey, executive director of Rhode Island Housing, the main government-sponsored housing agency for the state, says steady improvements in the slow-motion foreclosure crisis shouldn’t be expected before the second half of 2015—that is to say, two full years from now, while a degree of normalcy, with foreclosure rates back to typical historic levels, is still about five years away.

“There’s the human impact, there’s the community impact, and then there’s the financial impact” to the state’s economy, Godfrey says. “The biggest concern, of course, is what happens to these families.” The degree of emotional distress among borrowers reached the point that agency called in Samaritans of Rhode Island to give housing staffers suicide-prevention training.

In a sense, any numbers outlining the overall mortgage market understate the extent to which the mortgage crisis blew through low and lower-middle-income groups and neighborhoods, which were flooded with so-called subprime mortgages. Nationally, subprime loans—products with teaser rates, prepayment penalties, insurance fees, and other onerous features—saw foreclosure rates for adjustable subprime loans hit more than 20 percent, a staggering figure.

The problem of "underwater" mortgages

Christopher Rotondo, an organizer for DARE to Win, the community-advocacy group based in South Providence, says the crisis, rather than ending, appears to be entering a new phase. The first wave of foreclosures were largely the result of the defective and even predatory mortgage products zealously sold by mortgage lenders during the height of the housing bubble, 2004-2006, when nearly $2 trillion subprime loans were sold nationwide. Now, he says, those going through foreclosures are more likely to be people dealing with a follow-on affect of the crisis: the crash in home prices that left the value of their homes lower than the amount of their mortgage. The continued weakness in the state’s economy—with unemployment still over 9 percent—will further pressure this group.

A study, released in May by the Alliance for a Just Society, a coalition of community organizing groups, found that as of the end of last year, 11,000 Rhode Island homes were worth less than their mortgage—another category in which the state ranks last in New England on a per capita basis. Such so-called “underwater” mortgages are much more likely to go into foreclosure, as the families paying don’t have the option of selling the home to avoid having it seized by the bank.

Briggs is determined not to let that happen. She has already been through four attempts at loan modification, including one that turned out to be a loan scam that cost her $900, before one was successful in cutting her loan payments by slightly more than half, while stretching her mortgage out to 40 years. Still, she ‘s deeply underwater—the owner a property that a city estimate puts at about half the loan amount—and she’s working to get her principal reduced.

“I didn’t realize it was going to be this difficult,” she says. “It’s been a struggle. God has carried me all these years with this house, and I’m not going to lose it. I’m fighter.”