Michael Riley: GASB 68 Portends Huge Problems for City and State

Tuesday, June 17, 2014

In two weeks the fiscal year 2014 ends and fiscal 2015 begins for most if not all cities and towns in Rhode Island. Fiscal 2014 was a very positive year for equities both domestic and international. Fixed income markets were less helpful and generally represent 30 % to 40% of plan assets. The State of Rhode Island and the city of Providence had very positive results for Fiscal Year 2014.

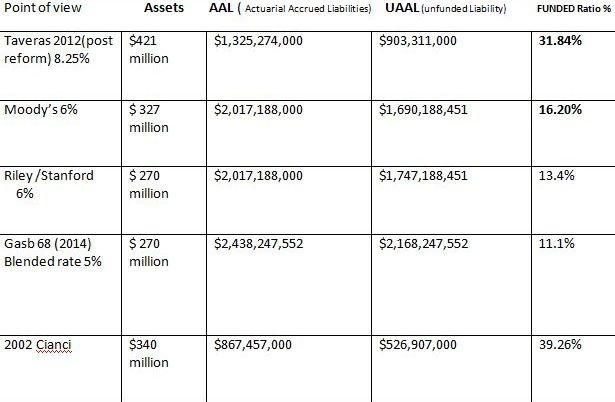

Through April 2014, Providence reported a trailing on year return of 13.4%, exceeding its discount rate of 8.25%. Providence has a high risk portfolio with more than 70% invested in equities and vulnerable to any downturn in the markets. We estimate Providence is approximately 20% funded and GASB 68, which goes into effect now, would force Providence to use a discount rate of (20% * 8.25%)+(80%*3.4%) or 4.37%.

As of April 2014, the State of Rhode Island pension plans had trailing one year returns of 11.87%, exceeding its discount rate of 7.5%. The state portfolio is significantly less risky than Providence’s portfolio with an approximately 62% weighting in equities and would very likely outperform Providence in any difficult environment. The state provides detailed analysis of its portfolio and risk metrics such as standard deviation of portfolio returns vs the benchmark portfolio and Sharpe Ratios.

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLASTThe State now reports assets of $8.06 billion & pension assets (as of June 2013) of $6.1 billion, while Providence reports assets of $272,848,000, which is well below the market value of assets at the beginning of the fiscal year of $393,100,000, as measured by Segal Consulting. So Providence lost $121,000,000 in pension assets and claims a 13.4% gain? How can that be? We’ve been asking that same question for well over a year.

Here is what we think is going on in Providence: First, about $57 million in last year’s assets was essentially a lie. This lie has been carried forward for some time, probably as far back as Cicilline. Taveras decided to carry on the lying tradition but he has a problem, his actuary warned in January 2014 (far after we did) the following:

Segal Report January 31, 2014

“As in prior valuations, the actuarial value of assets and the market value of assets include the discounted contribution paid by the city for the following year. We recommend that future valuations exclude discounted contributions from reported assets.” That amount was $57.3 million.

With ARC now representing roughly $70 million for fiscal 2015 but actual contributions well short of that number and Benefits paid out each year approaching $100 million Providence is extremely vulnerable. Two years of flat to down plan returns would essentially bankrupt the pension fund. One year like 2008 and it’s all over for the pension plan. Ironically, a bankrupt plan where no retiree gets a pension and where active workers assets are stripped to zero actually helps Providence from the point of view of liquidity and maybe even credit ratings. Due to a recent Rhode Island Law in 2011, bond holders have first lien on Tax revenue so they don’t lose a dime even if every city employee is stiffed or fired.

So Providence really only has assets of $273 million and liabilities of $1,212 billion (using 8.25%). Enter GASB 68 and Moody’s who will measure the liabilities as below 6%. The GASB 68 adjustment has been in the pipeline for years and every city town and Mayor has been briefed. Few, however, have told their constituents the truth. The RI Pension Commission talks about the rules but its Chair has violated the letter and spirit of the law and I believe is subject to SEC investigation or Judicial investigation in defrauding West Warwick voters. So here is the correct calculation for Providence assets and Liabilities and unfunded liability.

PROVIDENCE RI

Assumptions

Gasb 68 discount rate 4.37% 15 year maturity, current plan assets $272,848,000

Providence reported liabilities at 8.25 %= $1.212 billion

GASB 68 calculation

Step 1 adjust liabilities to proper discount rate

=1212000000*((1.0825^15)/(1.0437^15)) or $2,095,491,000 total liability

Step 2 Subtract assets set aside to fund liability

Assets = $272,848,000 (after eliminating account irregularity of 57 million)

Step 3 Calculate Unfunded liability

Assets – liability = net fundedness (or Unfunded Liability)

$273 million – $2.095 billion = Providence : $ 1.822 billion = UAAL = Pension Debt

This calculation shows that Mayor Taveras and the city of Providence, using a combination of illegitimate asset accounting and an inappropriate discount rate, have purposely understated the pension liability by approximately $1 billion Dollars.

Providence repeatedly uses bad data in the media and uses misleading analysis. The press such as WPRI and PROJO dutifully report these as fact. They are not facts. I did not make up GASB 68, I did not make up the fact their own auditor identified $57.3 million is phony assets.

Providence Pension Fact: after 5 years of one of the greatest bull markets ever and with Providence pretty fully invested, the pension plan has the same amount of assets it had in 2009. The plan is simply unsustainable and vulnerable to implosion within 2 years. That is not the impression the Taveras Administration gives and given the status of other cities and towns across Rhode Island, Mr. Taveras does not appear to even recognize the crisis, much less have the desire to address it. As a member of the Pension Crisis Commission he has missed 80% of the meetings and 25 in a row.

The State of Rhode Island, in comparison, is funded at approximately 60% using their 7.5% discount rate. There are no unusual accounting devices to overstate assets. These figures also assume the 2011 RIRSA reforms are unchanged. Using GASB 68 the State Calculations are as follows:

State of Rhode Island

As of June 30, 2013, discount rate =7.5%

Assets = $6.16 billion Liabilities = $10.60 billion >> UAAL = $4.44 billion debt

Gasb 68= (.6*7.5)+(.4*3.4)= 5.86%

Liabilities reported at $10.6 billion

Step 1 adjust liabilities to proper discount rate

= 10600000000*((1.075^15)/(1.0586^15))or $13,349,176,775 total liability

Step 2 Subtract assets set aside to fund liability

Assets = $6.1 billion

Step 3 Calculate Unfunded liability

Assets – liability = net fundedness (or Unfunded Liability)

$6.1 billion – $13.3 billion = $ 7.2 billion UAAL = Pension Debt

USING GASB 68 increases the current State of Rhode Island Unfunded Liability by $2.7 billion.

Combined with unwinding RIRSA 2011(estimated 4.2 billion) we estimate a net increase in Liability of nearly $7 billion.

The new funding ratio would be 35%.

If RIRSA is upheld the Funding Ratio will still drop to 45.8%.

Neither Gina Raimondo or Angel Taveras has been honest about GASB 68. You have been warned.

Michael G. Riley is vice chair at Rhode Island Center for Freedom and Prosperity, and is managing member and founder of Coastal Management Group, LLC. Riley has 35 years of experience in the financial industry, having managed divisions of PaineWebber, LETCO, and TD Securities (TD Bank). He has been quoted in Barron’s, Wall Street Transcript, NY Post, and various other print media and also appeared on NBC news, Yahoo TV, and CNBC.

Related Slideshow: Providence Pension Liability

A new report shows that Providence’s pension fund—even after the recent reform—is still in trouble. The below slides break out the key numbers for the pension fund, including the unfunded liability, the assumed and actual rates of return, the current level of benefits, and how long it will take the city to pay off the unfunded liability. Figures are current as of July 1, 2013 and are taken from the new Jan. 31 actuarial report from Segal Consulting.

2013.png)

.png)

2013_80_80_c1.png)

_80_80_c1.png)

Related Articles

- Michael Riley: Analysing A Crisis

- Michael Riley: The Municipal Pension Study Commission Is A Failure

- Michael Riley: The Pension Study Commission Needs To Face Reality

- Michael Riley: The Harsh Reality of the Pension and OPEB Crisis

- Riley: RI Ignoring The Financial Disaster Staring It In The Face

- Michael Riley: Is the RI Pension Commission Making Up Numbers?

- Michael Riley: West Warwick Is Headed For Disaster

- NEW: Riley Concedes, Warns RI Headed for ‘Disaster’

- Guest MINDSETTER™ Mike Riley: Right-to-Work is Right for Rhode Island

- Guest MINDSETTER™ Mike Riley: Rhode Island is More Conservative than You Think

- Riley: Providence Debt is Epic Disaster, Other RI Towns Even Worse

- Michael Riley: Providence Vying for Worst Funded City in America

- Michael Riley: These RI Cities + Towns Could Be Next in Bankruptcy

- Michael Riley: Don’t Pay

- Michael Riley: Municipal Pension Commission Comes Unglued

- Michael Riley: Failed Pension Commission Ponders Permanent Oversight Commission

- Michael Riley: West Warwick and Gallogly Pull Hoax on Taxpayers

- Michael Riley: 38 Studios Insider Trade and Municipal Fraud

- Michael Riley: State Pension Fix in Limbo as Municipal Debt Grows

- Riley: Cranston and Mayor Fung Play the Hand that was Dealt

- Michael Riley: Moody’s Lowers the Bomb…Look Out Rhode Island

- Michael Riley: Taveras and Polisena No-Shows at Pension Commission

- Michael Riley: RI Municipal Pension Study Comm. Is in Failure Mode

- Michael Riley: Rhode Island’s Potential Pension Nightmare