Top Ten Local Pension Plans in Crisis

Monday, January 16, 2012

Two thirds of all the locally administered pension plans are now in financial dire straits after the total cost of the unfunded liability for municipal retirement plans ballooned by more than a billion dollars in a year, according to data obtained by GoLocalProv.

Between spring 2010 and fall 2011, the total unfunded liability for local retirement plans swelled from $4.3 billion to $5.6 billion, according to the state Auditor General. Currently local pensions are collectively 43 percent unfunded, at an amount that stands at $2.1 billion. But that’s not even half the problem: the remainder of the unfunded liability stems from what is owed for retiree health care, which is $3.5 billion (technically known as Other Post Employment Benefits, or OPEB).

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLAST‘Ticking time bomb’

“The state is facing a ticking time bomb with the magnitude of the unfunded liabilities in these locally run plans,” said Harriet Lloyd, executive director of the Rhode Island Statewide Coalition (RISC). “The new year has begun with communities like East Providence, Woonsocket and Pawtucket facing deficits they can’t overcome and the report shows there are additional communities with huge retirement liability problems.”

Lloyd said the data underscores the need for the new Municipal Pension Study Panel formed last week to “confront the fact that the tab for pensions and health benefits cannot be met” as it currently stands.

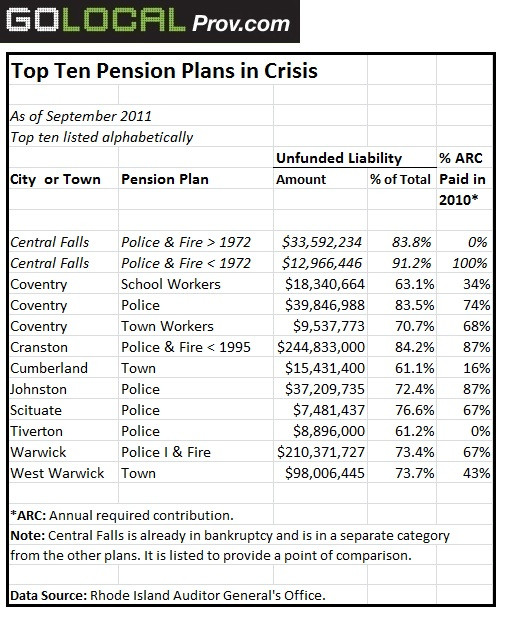

Topping the list of troubled retirement plans is Central Falls, which the Auditor General has put in a category of its own because it is in bankruptcy and its pension funds are nearly insolvent.

The other communities that made the top ten list of pension plans in crisis are not only significantly underfunded, at less than 60 percent, but also not making their annual required contributions (ARCs) that actuaries say are necessary for a pension fund to be financially viable over the long term. (See chart.)

The top ten list includes several communities that have already made headlines for their pension troubles—Cranston, Johnston, Warwick, and West Warwick—as well as others that have not, such as Coventry, Cumberland, and Tiverton. Two other communities that are lagging in their annual contributions, but whose unfunded liability is not as large as the top ten are the Westerly pension fund for police and the East Providence fund for fire and police.

In addition, ten more local pension funds fall into two groups: either they are significantly unfunded but they are catching up by making 100 percent of their annual required contributions or their plans are well-funded but they are falling behind on their annual contributions.

Those communities include well-known fiscally stressed communities like Providence, Pawtucket, and Woonsocket as well as some that are a bit surprising, like Narragansett and Smithfield. (See below charts for full list.)

Broad impact on communities

The new data shows the sweeping extent to which the future pension obligations are straining local budgets:

■ Crippling cuts to benefits: The fate of Central Falls municipal retirees, who saw their pensions chopped in half, is well known. But similar drastic measures are not inconceivable for communities like Cranston, where the city’s fire and police pension fund will run out of funds to pay pension benefits to retirees in about two years. Close behind is West Warwick’s, where benefits will run dry within the next decade, according to the Auditor General.

■ The pension tax: Last year, GoLocalProv reported that about half of property taxes in Providence were owed to its retirement system. But now, Providence is not alone. Woonsocket, Central Falls, and Johnston owe 61 percent, 58 percent, and 47 percent, respectively, of their property taxes to their retirement systems. Overall, one out of every four dollars in local property taxes collected in Rhode Island should be going to local retirement plans, according to the Auditor General.

■ Bond ratings: Five out of seven communities that recently had their bond ratings downgraded had the health of their pension funds cited as a factor in the decision. Those communities are: Central Falls, Coventry, East Providence, Providence, and West Warwick. All of them had had their pension plans previously identified as at-risk by the Auditor General. Lower bond ratings make it harder to borrow money, putting yet another strain on local budgets.

‘There is no money left’

Communities are already bracing themselves for the enormous task of how to turn around their pension funds. “It’s not going to be an easy quick cure,” said Kerry McGee, the vice president of the town council in Coventry.

“There is no money left. I don’t know how we’re going to do it,” McGee added. “We have a tough, tough budget cycle coming up. You either cut services or you raise taxes. We don’t want to do either one of them.”

McGee said local officials have already met with Governor Lincoln Chafee and state Treasurer Gina Raimondo over the status of their pension funds. And, he said the town is in the early stages of developing a five-year plan for boosting its annual payments to its retirement system to 100 percent of what is required—such plans are a new mandate instituted by the General Assembly last year.

In Central Falls, where severe tax hikes have already been implemented, city councilman James Diossa said residents cannot afford any more, especially when more than half of the property tax levy is already owed to the retirement system. “It’s a very huge concern because we can no longer tax our way out of it,” Diossa said.

Warwick unfunded liability: $200 million plus

Of the top ten most troubled pension plans, Warwick’s fund for police and fire is saddled with the largest unfunded liability, which stands at $210.3 million. The city is currently almost halfway into a 40-year amortization schedule for its pension fund, which is not consistent with the standards of the Governmental Accounting Standards Board, which normally calls for a 30-year period.

Mayor Scott Avedisian told GoLocalProv that the impetus for re-amortizing will have to come from state officials.

“I have spoken with the Auditor General about the fact that we have a 40-year funding cycle that started 18 years ago, long before the other cities and towns began dealing with their pensions,” Avedisian said. “I have told the Governor, Treasurer, and Auditor General that if they want me to re-amortize that pension plan for 30 years instead of the 22 years that are left, they need to tell us that and we will ask the city council for approval.”

Avedisian did praise state officials for the appointments they made to the new municipal pension panel. “The members that have been announced represent a broad spectrum of perspectives and interests. I am happy to see that Mayors Fung, Taveras, and Polisena and Town Manager Kaiser [in Jamestown] will represent local government,” Avedisian said. “They bring years of experience to the discussions and deliberations of the commission.”

Debate over solutions begins

One of the panel members, Paul Doughty, head of the Providence Firefighters, is approaching his work with a simple maxim: “My priority is sort of along the Hippocratic Oath… First do no harm,” Doughty said. In other words, while the panel is doing its work, it needs to make sure that the fiscal health of local pension funds does not get any worse.

The next task for the panel is to figure out how to get local pension plans to a stable level of funding. Below 60 percent, the Auditor General considers pension plans significantly underfunded, while 80 percent was the ideal target set for state pension funds in the reform legislation passed during the fall General Assembly session.

Lloyd outlined several options for how the state could get there. “COLA suspensions, greater health benefit co-pays by existing retirees, and moving all retirees into Medicare are among the reforms that the municipal plans must adopt if there is any hope to keep communities from fiscal collapse,” She said.

Doughty envisions three scenarios: solutions that are negotiated between affected workers and retirees and municipalities; solutions that are set by local ordinance or state legislation and lead to litigation; and solutions that emerge out of bankruptcy.

Bankruptcy—which led to the drastic pension cuts in Central Falls—is the least desirable of those outcomes, according to Doughty. “I think it’s a real injustice what happened to the retirees,” he said. “It remains my number one concern.”

A unilateral solution might appeal to local administrators but it could backfire if it ends up in court. Doughty pointed to the recent state pension reform legislation, which union officials have said is likely to lead to a lawsuit, or an expansion of an existing lawsuit. If the state saves $300 million each year but ultimately loses in court three years later, it would be on the hook for $1 billion, Doughty warns. “They need to understand they absolutely could lose and take some actions that are prudent,” he said. “I would say the same for any city or town.”

Putting saved pension money into an escrow account until all litigation has been exhausted, he said, would avoid financial disaster down the road.

A negotiated solution at the local level, he suggested, is the best outcome. And, he said the ultimate solutions should be worked out by cities and towns. “They got themselves into it. They can get themselves out of it,” Doughty said. “That’s not a sarcastic answer. They have more of a vested interest. There’s no interest like self-interest.” (He added that the state still has an important oversight role to play.)

Merger with MERS?

One idea that has been batted around recently: merging all the local pension plans into the state-administered fund for local workers, known as the Municipal Employees Retirement System, or MERS. Unlike the local plans, MERS is in much better financial shape and communities that are members must make 100 percent of their annual required contribution.

One advocate of the MERS merger is the Auditor General, Dennis Hoyle. RISC also backs the idea.

Local officials interviewed by GoLocalProv, however, are not quite ready to get on board. In Central Falls, Diossa said it was worthwhile to explore the idea and his counterpart in Coventry, McGee, agreed. “It sounds like a good idea, but a lot of the ideas given up by the state don’t affect our municipal pensions,” McGee said.

Doughty, for now, is opposed. “In a de facto way, it takes pensions off the table as a negotiated item,” he said, pointing out that merely moving local plans into MERS still does not address the main issue: how to fund them.

“I will keep an open mind,” he added. “It’s essential these systems remain solvent, however we get that.”

If you valued this article, please LIKE GoLocalProv.com on Facebook by clicking HERE