The Most Foreclosed Communities for 2012

Friday, March 15, 2013

The worst of the housing crisis may be behind it, but Rhode Island is still plagued with foreclosures that make the state the highest-ranking in the region, according to a new report issued by a local housing advocacy organization.

The number of foreclosures declined overall by 22.8 percent between 2011 and 2012, but Rhode Island nonetheless has the highest foreclosure rate in New England and is tied with Maryland for seventh place in the nation, according to HousingWorks RI.

Jessica Cigna, the research and policy associate at HousingWorks RI, said the improving numbers in Rhode Island were nonetheless encouraging. “It’s not a crisis, but still a problem,” Cigna said.

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLASTLast year, nearly one percent of the mortgaged housing stock in the Ocean State went into foreclosure, the new data shows.

“Rhode Island’s foreclosure risk is still high for the New England states,” said Ray Neirinckx, the Housing Resources Coordinator for the state Housing Resources Commission. “It reflects both the slow economic recovery and the persistence of the subprime lending that has disproportionately impacted our urban communities.”

Foreclosures increased in nine communities

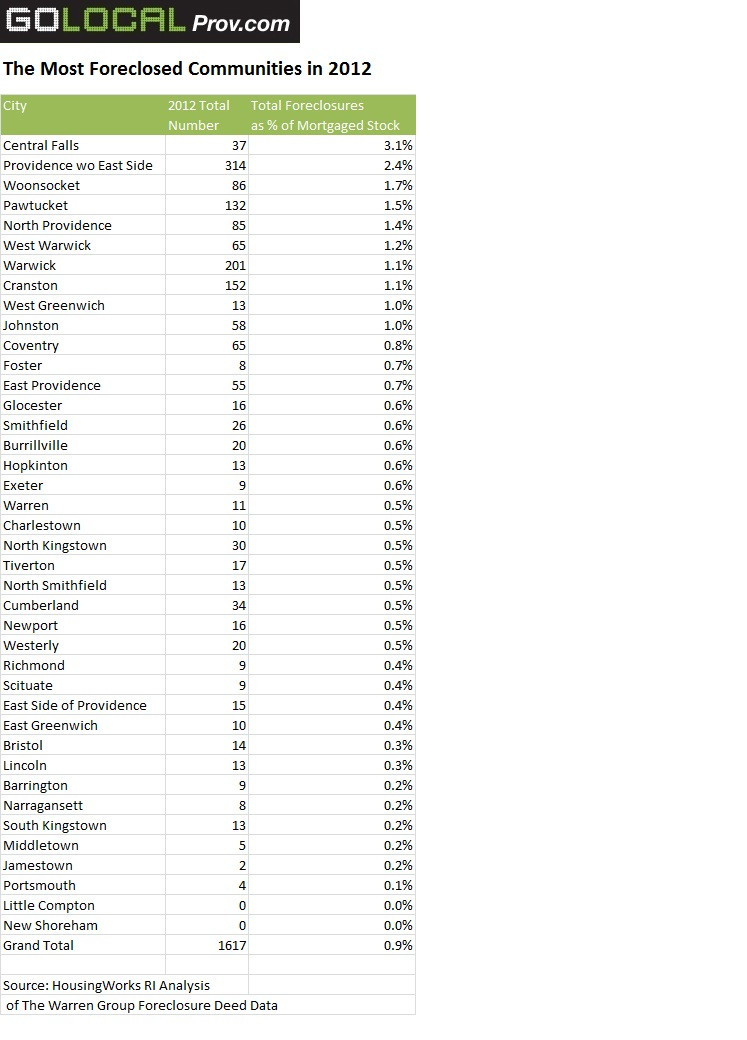

The communities hit hardest by foreclosures mirror those cities that persistently rank highest in the state for their fiscal troubles. The top four are: Central Falls, with 3.1 percent of its mortgaged housing stock sent into foreclosure last year; Providence excluding the East Side at 2.4 percent; Woonsocket, 1.7 percent; and Pawtucket, 1.5 percent. (See below tables.)

Other communities numbered among the top ten most foreclosed are: West Warwick, Warwick, Cranston, West Greenwich, Johnston, and Coventry.

The number of foreclosures between 2011 and 2012 declined in most cities and towns, even in the top ten that are hardest hit in the state.

However, in nine communities, the housing situation worsened last year: Exeter, Narragansett, Tiverton, Warren, Burrillville, Barrington, East Greenwich, Newport, and Smithfield.

High unemployment could hold back housing recovery

Cigna said foreclosures that are directly tied to the housing bubble are becoming less common. In 2009, 63 percent of foreclosures had deeds that originated during the housing bubble between 2000 and 2006. By comparison, 47 percent of the foreclosures in 2012 had deeds from that same period, according to Nicole Lagace, spokesperson for HousingWorks RI.

“So we cycled through the foreclosures because of the bubble and now the foreclosures we’re experiencing is in line with the unemployment rate,” Cigna said.

She suggested that the future of the housing market will be closely linked to the performance of the state economy, which continues to struggle with one of the highest unemployment rates in the country, despite recently dipping below 10 percent. With four in ten households allocating 30 percent of their income towards housing costs, unemployment makes homeowners especially vulnerable to foreclosure, Cigna said.

“We know that many homeowners are struggling,” she said.

In particular, the report found that:

■ The fourth quarter of 2012 saw an 11.2 percent drop in the filing of foreclosure deeds as compared with one year earlier and a 36 percent decrease from 2009.

■ The number of 2012 foreclosures is 43 percent less than 2009.

■ The .9 percent of housing stock that was in foreclosure represents a decrease from 1.13 percent in 2011.

Not all year-to-year indicators are positive. One red flag: 16,000 Rhode Islanders last year called a United Way hotline for preventing foreclosure, a 64 percent increase over 2011, according to Cigna.

City looking for ‘breathing room’

Providence city Councilman Luis Aponte said he was aware there were several reasons why foreclosures are reported to be declining. “That doesn’t change the condition of many neighborhoods where are large numbers of foreclosed and vacant properties,” Aponte said.

He said foreclosed properties that remain vacant become sites of vandalism and deterioration. He expressed hope that housing foreclosures would continue to drop, giving city officials and neighborhoods some “breathing room” to address the number of already-foreclosed and vacant houses that have contributed to urban decay in Providence.

“I’m hopeful that as the economy picks up people will be able to retain their houses,” Aponte said.

West Warwick still feeling brunt of foreclosures

West Warwick had 65 foreclosures in 2012, which translates to 1.2 percent of its mortgage stock—enough to make the community the sixth most foreclosed municipality in Rhode Island last year.

“West Warwick is a microcosm of what is going on in some neighborhoods in Providence,” said Kerry Anderson, the newly appointed West Warwick Building Official and a five-year veteran of the Building Department in Providence.

Anderson said homeowners are letting their properties fall into decline even before eviction. “If people can’t afford their mortgages, they just walk away today,” Anderson said.

In response to the burst in the housing bubble, financial institutions have adopted more stringent lending rules, limiting options for borrowers who need help and only making the housing crisis even worse in places like West Warwick, according to Anderson.

“It’s a spiraling, vicious cycle,” Anderson said. “It does perpetuate itself.”

He said most foreclosures he has observed involve multi-family properties where conflict often breaks out among landlords who are on the bad side of a loan and their tenants—forcing local building officials to intervene. Some landlords, he added, simply can’t keep up with tenants who trash their apartments. Others scrimp on maintenance out of greed, according to Anderson.

Experts weigh in on report

Like other economic indicators in Rhode Island, the foreclosure rate is improving but isn’t quite where state officials would want it to be.

“We are in a slow recovery. It’s been a poor recovery compared to recoveries after recessions in the 80s and 90s, but we are still slowly recovering,” said retired Brown University economist Allan Feldman, referring to both the state and the national economy.

Feldman said he was certain there are correlations between unemployment and foreclosures, but he said the most notable thing in the recovery is the “extremely aggressive” action of the Federal Reserve in driving down interest rates.

That helps borrowers, but the policy is also a dangerous one, Feldman added.

He said interest rates can’t go down much further because they are already so close to zero. He expects that interest rates will rise and eventually reach the 4 percent to 6 percent levels that were at a few years ago.

“If that happens, that’s bad news for the real estate market,” Feldman said.

Beyond the Federal Reserve, credit for the foreclosure reduction should also go to local housing agencies, added Neirinckx.

“It is a testament to our under-funded counseling agencies and the exceptional work done with the State’s Hardest Hit Fund (HHF) administered by Rhode Island Housing,” he said. “It reflects the slow success of the National Settlement with the five larger mortgage servicers and the Independent Foreclosure Review that has been replaced by the new Federal Reserve and Office of Comptroller of the Currency (OCC) order with ten mortgage servicers.”

Solutions may be elusive

The executive director of HousingWorks RI, Nellie Gorbea, called on state policymakers to make lower housing costs one of their top priorities. “It’s essential for policymakers to consider how high housing cost burdens affect not only Rhode Islanders, but our local economies when developing policies to promote economic growth,” Gorbea said.

HousingWorks RI has advocated for housing bonds as a way to ease such high costs. The most recent bond, for $25 million over two years, passed in the last election.

Neirinckx also argues that the state’s performance with the Hardest Hit Fund should “result in additional funding” so housing retention efforts can be expanded.

In West Warwick, however, Anderson suggested that solutions to the foreclosure crisis may remain elusive. He said a number of different factors are driving the problem, with no single one contributing more than the others. “It’s a problem that is many-faceted,” Anderson said. “I don’t think there is a fix that can be solved by any one idea.”

If you valued this article, please LIKE GoLocalProv.com on Facebook by clicking HERE.

Related Articles

- Former BankRI CEO Lands $300/Hour Gig Mediating Foreclosures

- NEW: State to Receive Additional $634,000 in Foreclosure Prevention Funds

- Timeline: The Steps Leading to the Foreclosure Crisis

- Attorney General Patrick Lynch Joins Nationwide Foreclosure Fiasco Investigation

- Guest MINDSETTER™ Jay Harding: How to Save your Home from Foreclosure

- NEW: Whitehouse Urges Mortgage Regulator to Adopt New Approach to Foreclosure Crisis

- Tom Sgouros: More Accountability Needed in Foreclosure Crisis

- Banks Cash in on Foreclosures in Providence

- HousingWorks RI: State Has Highest Foreclosure Rate in Region

- Foreclosure Rate Drops in Rhode Island

- Investigation: 5 Banks Accused of Fraudulent Foreclosures

- RI Loses $5.6 Billion to Foreclosures

- Foreclosures Sold at 30% Discount in First Quarter 2010

- NEW: Family Sit-in Fights Wells Fargo Foreclosure

- RI’s Foreclosure Crisis - City by City Breakdown

- Foreclosures Still Rock RI Each Month

- NEW: Kilmartin and Taveras to Host Foreclosure Workshop

- State House Report: Compassion Centers, the Landfill & Foreclosure Protection

- Foreclosures Up 19 Percent

- NEW: Kilmartin to Sign Joint State-Federal Mortgage Servicing and Foreclosure Settlement

- State Report: Gay Marriage Battle, Foreclosure Crisis & the Sawyer School

- Foreclosures in RI Fall 25.2% from This Time Last Year

- NEW: Rhode Island to Recieve $172 Million from Landmark Foreclosure Settlement

- Taveras Promises to Tackle Providence Foreclosure Crisis