Lardaro Report: Good Economic News Becoming More Difficult to Find

Monday, May 12, 2014

In his most recent report, URI Economist Len Lardaro presents a disappointing stagnation in economic indicators, and notes that foul weather no longer lingers as an excuse.

Lardaro states, "It appears that our negatives are going to strengthen in the coming months, which will increasingly offset our ongoing positives, leading to a bumpy ride as 2014 progresses. All we can do is hope that increasing national momentum will moderate this potential slowing of our state’s momentum."

Lardaro's Current Conditions Index:

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLASTThe much anticipated bounce back from the adverse effects of the harsh February weather turned out to be a non-event. While the indicators most obviously impacted by the weather improved as expected, several other indicators were far less accommodating, leaving the March Current Conditions Index stuck at the same value it attained in February, 58. Unfortunately, this extended the string of consecutive months where the CCI has failed to improve relative to its year-earlier value to eight.

New home construction, which came to a virtual standstill last month, returned to a more reasonable level. And Retail Sales, which should have felt weather effects, remained strong for both February and March. As we move farther beyond the uncertainties produced by winter weather, the underlying performance of Rhode Island’s economy is becoming more apparent. While the overall picture that emerges is mixed, we appear to have entered a period where our negatives are beginning to expand, increasingly offsetting the beneficial effects of the parts of our state’s economy that continue to exhibit strength. The result will be a period of yet slower growth overall which will at times mask a some or a great deal of the positive momentum that exists within our state. While this is hardly the outcome we wanted to observe, it indicates that we can expect the present recovery to become even less broadly based should these trends persist. The good news, which is becoming more difficult to find, is that an accelerating rate of growth for the national economy will clearly benefit Rhode Island as we move through the remainder of 2014. How much we benefit, however, is a very different question. We may well see improvements in absolute terms (like the recent decline in our Unemployment Rate), but relative to other states, we will continue to lag (we remained #1 for joblessness in March).

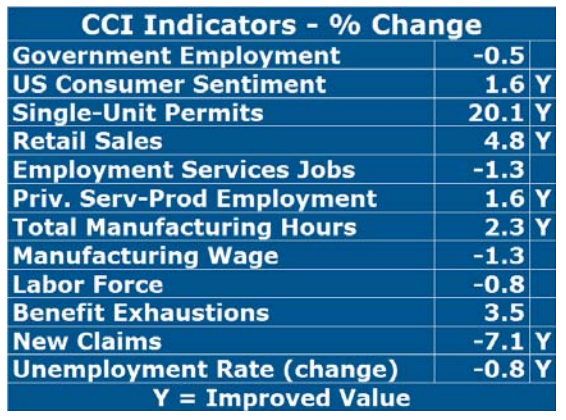

For March, four of the five leading indicators contained within the Current Conditions Index improved, some by healthy rates. Single -Unit Permits, which reflect new home construction, the indicator most adversely impacted by winter weather last month, bounced back with a 20.1 percent increase in March (returning to around 70 permits per month). New Claims for Unemployment Insurance, is the timeliest measure of layoffs, also turned in a strong performance, falling by 7.1 percent relative to last March. At present, it is not clear whether this indicator will resume its previous downtrend. Should it fail to, it would impart a decidedly negative bias to the momentum that exists at present. Total Manufacturing Hours, which measures strength in our manufacturing sector, sustained its strength in March (+2.3%), as a rise in employment offset the negative effect of a slight decline in the length of the workweek. US Consumer Sentiment rose by only 1.6 percent, but this was its fourth increase following three consecutive months of declines. The final leading indicator, Employment Service Jobs, which includes temporary employment and is a prerequisite to employment growth, fell 1.3 percent in March, its fourth consecutive decline. Let’s just say I continue to view changes in this indicator suspiciously.

Retail Sales turned in yet another strong performance in March, rising by 4.8 percent relative to a year ago. Keep in mind this indicator excludes clothing sales, which likely grew substantially in light of March’s cold weather. Private Service- Producing Employment, which was revised higher in the recent rebenchmarking, continues to display strength, increasing by 1.6 percent relative to last March. The performance of our state’s Labor Force continued as it has for a while now. The “good news,” was that its rate of decline fell below one percent. In spite of this, March was its eleventh consecutive decrease. Even with these declines, Rhode Island once again claimed the #1 jobless slot in March, as our Unemployment Rate fell all the way to “only” 8.7%. Benefit Exhaustions, w hich reflects longer-term joblessness, rose in March (+3.5%) for the first time in over a year. Finally, Government Employment fell by 0.5 percent to just under 60,000.

THE BOTTOM LINE

The present recovery continues to be less broadly based than it was a year ago based on the fact that the CCI has now failed to exceed its year-earlier value for eight consecutive months. Winter weather is no longer a possible explanation. While a number of areas continue to display strength, and can be expected to continue doing so in the coming months, it appears that our state’s cyclical negatives are gaining strength, which will dissipate our overall momentum. The critical question at present continues to be whether increasing nation- al economic momentum will be sufficient to help us fend off the ef- fects of our strengthening negatives.

Related Slideshow: 7 Strategies for Rhode Island Economic Development in 2014

What will it take to move the Rhode Island economy forward in 2014? GoLocal talked with elected officials, candidates, and leaders for their economic development plans in the coming year.

Below are key elements of the economic priorities for Governor Lincoln Chafee, Speaker of the House Gordon Fox, Senate President M. Teresa Paiva-Weed, House Minority Leader Brian Newberry, gubernatorial hopefuls General Treasurer Gina Raimondo and Ken Block, and RI Center for Freedom and Prosperity's Mike Stenhouse.